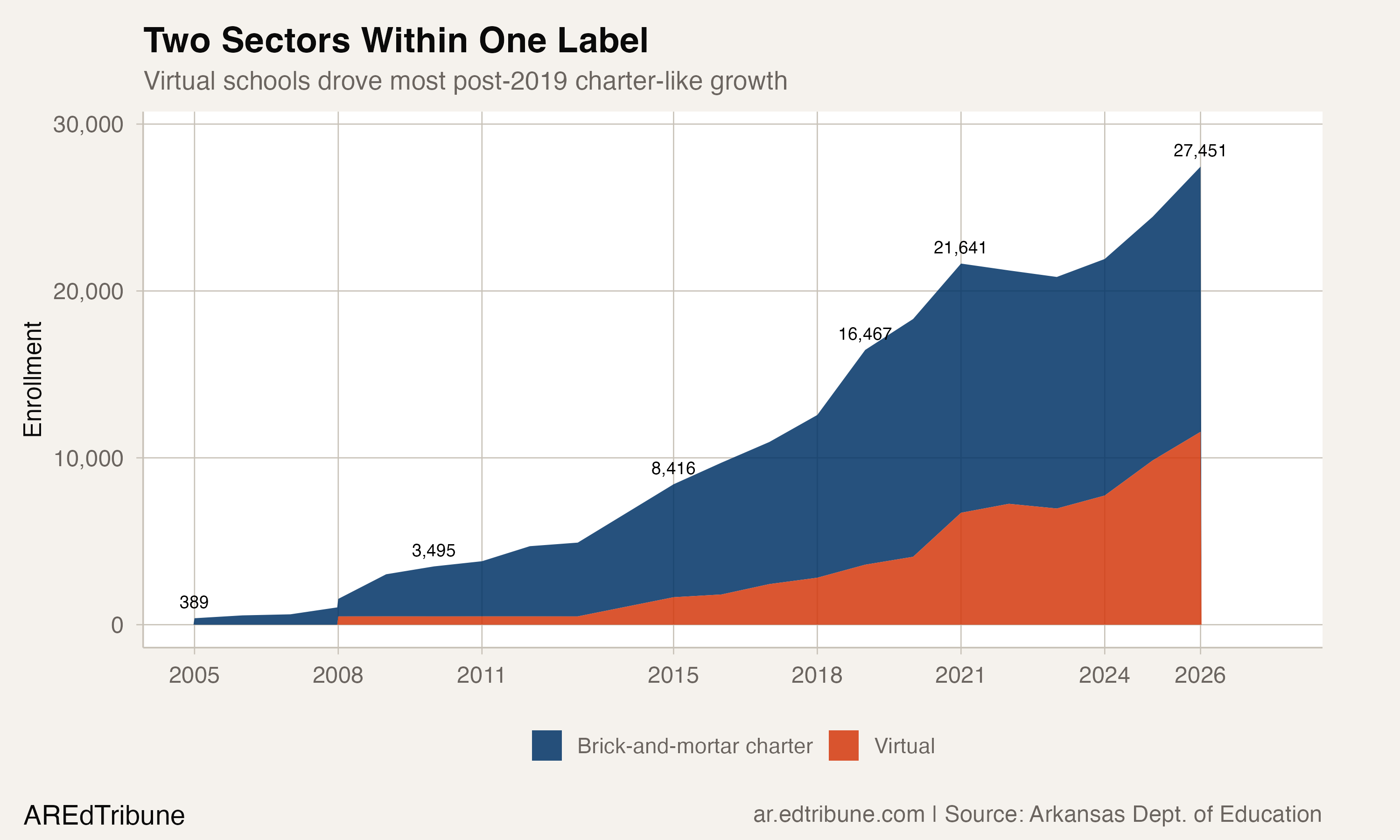

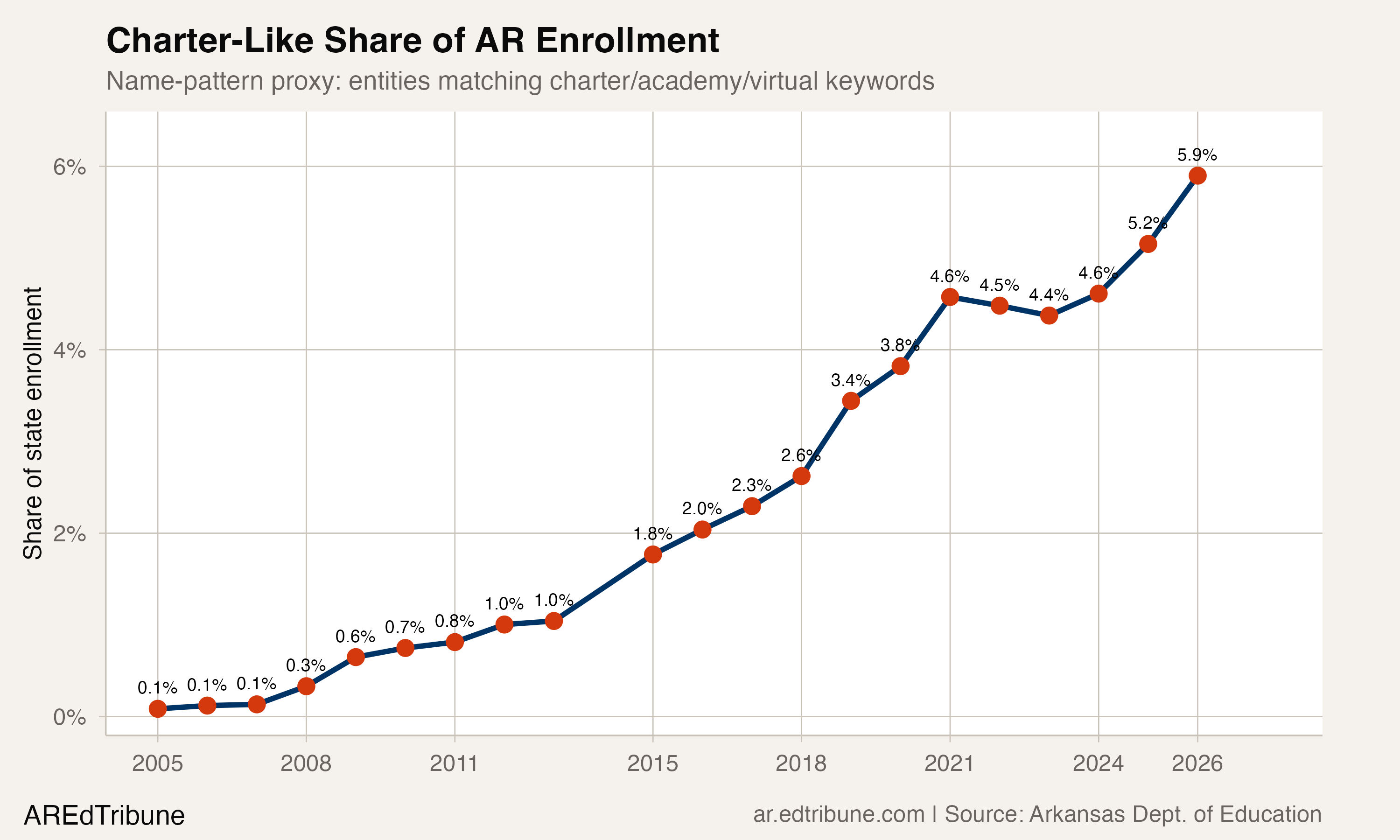

Arkansas does not track charter schools with a formal flag in its enrollment data. Identify them by name, though, and the pattern is unmistakable: 17 entities matching charter, academy, and virtual keywords enrolled 27,451 students in 2025-26, up from 8,416 across 14 entities in 2014-15. Their share of statewide enrollment has more than tripled, from 1.8% to 5.9%.

That growth happened while the state's overall enrollment fell by 10,662 students. Traditional districts lost 29,697. The arithmetic is exact: traditional districts lost 19,035 more students than the statewide total declined. The charter-like sector gained 19,035. Whether those are the same students, or whether both trends have independent causes, the data cannot say.

A methodological caveat up front

The Arkansas Department of Education does not publish a charter school flag in its enrollment-by-race dataset. The analysis here uses a name-pattern proxy, matching entities whose names include terms like "charter," "academy," "virtual," "eStem," or "Haas Hall." This captures the universe of open-enrollment charters and virtual schools but is inherently approximate. Imboden Charter School District↗ET, for instance, is a traditional district that happens to carry "charter" in its name (53 students). Its inclusion does not materially change the sector totals.

All enrollment numbers come from the ADE Data Center. The sector labels are the analysis's own classification, not the state's.

Two sectors hiding inside one label

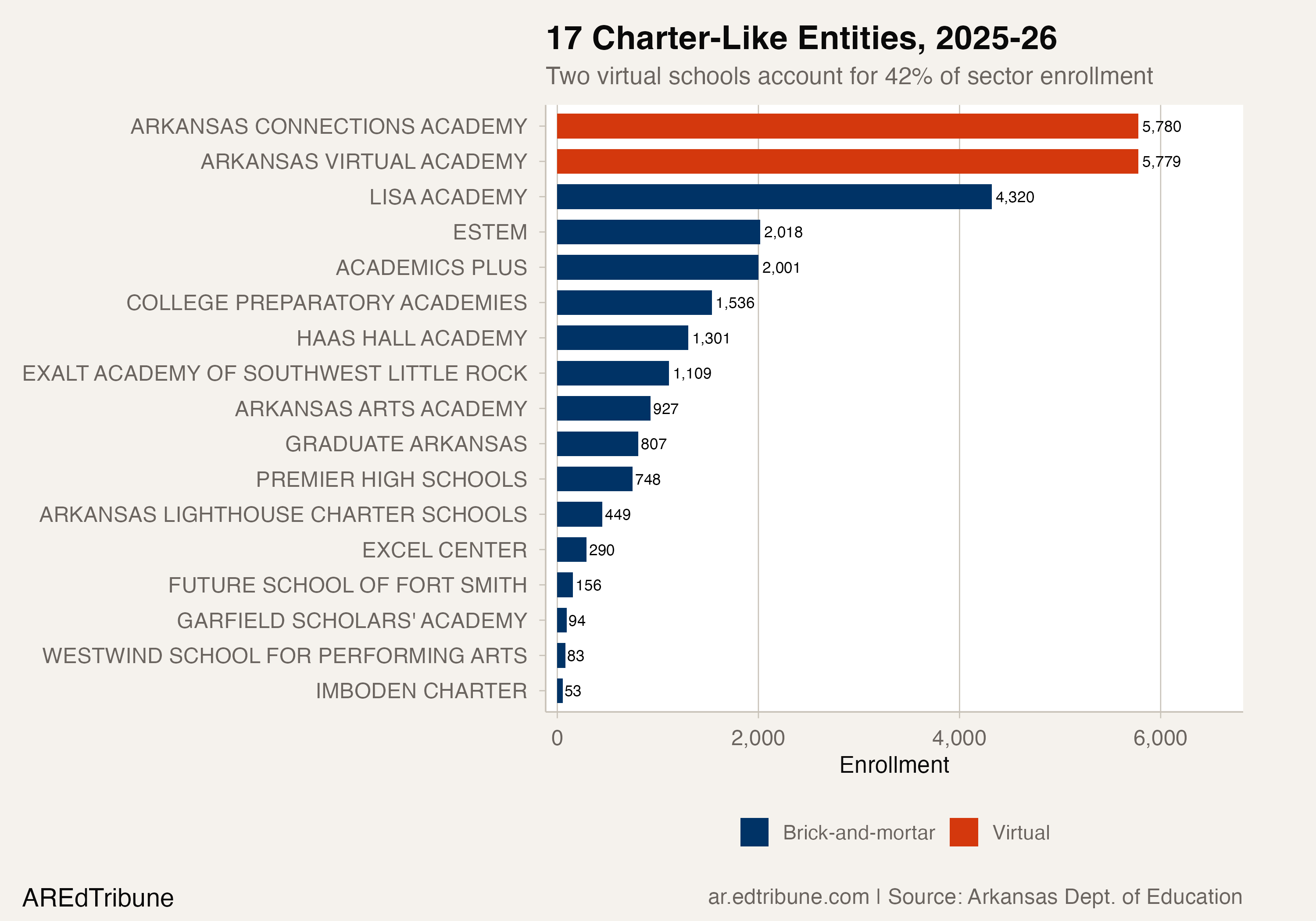

The 5.9% headline number conceals a structural split. Of the 27,451 students in charter-like entities, 11,559 attend just two virtual schools: Arkansas Connections Academy↗ET (5,780) and Arkansas Virtual Academy↗ET (5,779). Together they account for 42.1% of the sector's enrollment.

The brick-and-mortar side, 15 entities enrolling 15,892 students, grew at a steadier pace. Virtual enrollment is the volatile component. Arkansas Virtual Academy sat at a flat 499-500 students from 2008 through 2013, suggesting a regulatory cap. By 2015, it had jumped to 1,647. Connections Academy launched in 2016-17 with 343 students; eight years later it enrolls 5,780.

The COVID-19 pandemic accelerated the virtual side. Between 2018-19 and 2020-21, virtual enrollment in the two schools surged from 3,597 to 6,708, an 86.5% increase. Brick-and-mortar charters grew 16% over the same period. Virtual enrollment dipped slightly in 2022 and 2023 as the pandemic receded, then resumed climbing: 7,741 in 2023-24, 9,844 in 2024-25, and 11,559 in 2025-26.

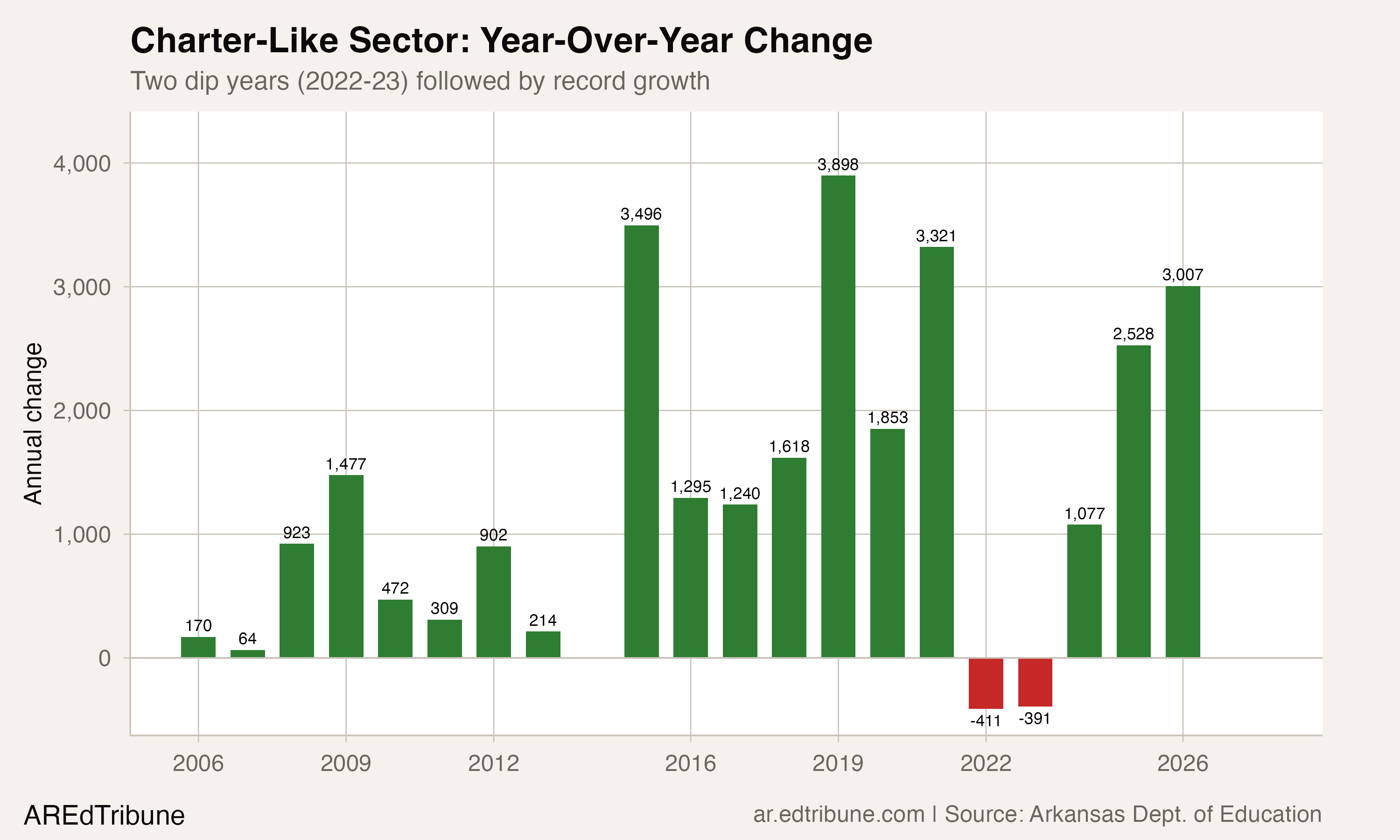

The growth trajectory is not smooth

The sector as a whole actually shrank in 2021-22 and 2022-23, losing 411 and 391 students respectively. That contraction reflected real churn: seven entities present in 2018-19 had disappeared from the data by 2025-26, including Little Rock Preparatory Academy (361 students in 2019), Haas Hall Bentonville (419), and Pine Bluff Lighthouse Academy (273).

The dip proved temporary. The sector added 1,077 students in 2023-24, then 2,528, then 3,007 in 2025-26, the largest annual gain since 2019. The acceleration coincides with the LEARNS Act, signed by Governor Sarah Huckabee Sanders in March 2023, which removed the cap on charter school authorizations and created the Education Freedom Account voucher program.

Who attends charter-like schools

The charter-like sector serves a different demographic mix than traditional districts. Black students make up 23.7% of charter-like enrollment but 18.8% of traditional enrollment. Asian students are 5.2% versus 1.8%. White students are 47.7% of the charter-like sector, compared with 57.1% of traditional districts. Hispanic enrollment is roughly equal in both sectors (15.9% vs. 15.4%).

LISA Academy↗ET, the largest brick-and-mortar charter network at 4,320 students, is STEM-focused and has expanded to 10 campuses across the state, including a hybrid model launched in 2021. It has grown from 163 students in 2004-05 to become the sector's third-largest entity.

eStem Public Charter School↗ET tells the opposite story. After peaking at 3,202 students in 2019-20 (when three separately reported campuses had consolidated under one LEA code), it has declined to 2,018, a 37.0% drop in six years. The decline accelerated after 2022, losing 150 to 380 students annually.

The LEARNS Act and the new competitive landscape

The LEARNS Act reshaped Arkansas school choice in three ways relevant to charter enrollment. First, it removed the numerical cap on open-enrollment charter authorizations. Second, it directed poorly performing districts to partner with charter operators. Third, it created Education Freedom Accounts, which by 2025-26 had approved nearly 47,000 participants, at a projected cost of $327 million.

The EFA program is distinct from charter enrollment. EFA funds flow to private schools and homeschool families, not to public charter schools. But the two programs share a policy ecosystem. The cap removal encourages new charter openings; the voucher program signals a broader shift toward family choice that may accelerate transfers from traditional districts to all non-traditional options.

"95 percent of them already were attending private schools, so this was just an additional expense for the Arkansas taxpayer." — April Reisma, president of the Arkansas Education Association, via KATV, Jan. 2026

That critique applies to the EFA voucher program specifically, not to charter growth. But it underscores the difficulty of disentangling true transfers from enrollment that was never in public schools to begin with.

What traditional districts are losing

The 29,697-student decline in traditional districts since 2014-15 is not spread evenly. Pulaski County Special School District↗ET lost 5,081 students (30.6%), Little Rock School District↗ET lost 4,399 (18.8%), and Pine Bluff↗ET lost 1,582 (37.3%). Delta and southeastern districts bore disproportionate losses.

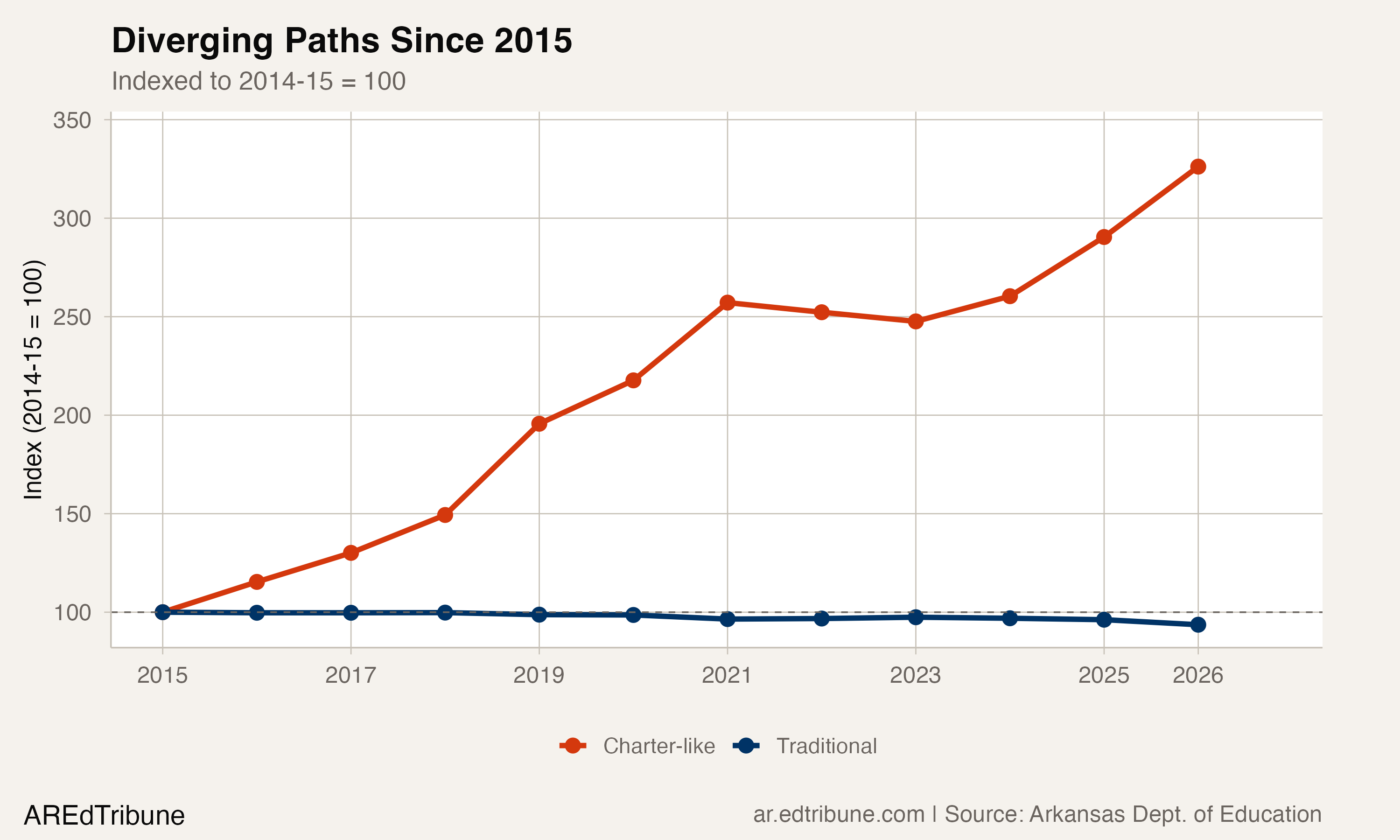

The divergence chart indexed to 2014-15 tells the story: traditional enrollment has drifted steadily downward to 93.6% of its baseline while charter-like enrollment has risen to 326.2%. But the absolute numbers matter. The traditional sector still enrolls 437,970 students, 94.1% of the state total. The charter-like sector, for all its growth, remains small.

Northwest Arkansas is the one region where traditional districts are growing. Bentonville↗ET added 4,447 students since 2014-15 (+28.7%), driven by population growth in the Walmart headquarters corridor. Fayetteville, Pea Ridge, and Farmington also gained. The charter-like entities with Northwest Arkansas roots, Haas Hall Academy and Arkansas Arts Academy, have also grown, but the traditional districts in that region are gaining students on net.

What comes next

At 5.9%, Arkansas's charter-like sector is still smaller than the national average for states with mature charter laws. The LEARNS Act's removal of the charter cap creates room for further growth, and as many as 18 new charter applications were in the pipeline for 2024-25. If even half succeed and reach scale, the sector could approach 8% within a few years. Whether virtual schools, which have added 7,962 students since 2019, continue to drive that growth or brick-and-mortar operators catch up will determine what "charter growth" actually means: more physical schools in communities, or more students learning from home.

Detailed code that reproduces the analysis and figures in this article is available exclusively to EdTribune subscribers.

Discussion

Sign in to join the discussion.

Loading comments...